What You Need to Know About Mortgage Penalties Before You Switch or Break Early

Why This Post Could Save You Thousands

You’ve likely heard that breaking your mortgage comes with a penalty — but most homeowners don’t fully understand what that penalty is, how it’s calculated, or whether breaking is actually a bad thing.

Here’s the truth:

💡 Sometimes paying the penalty is the smartest financial move you can make.

In other cases, it’s not worth it — but you won’t know unless you actually run the numbers.

Many banks rely on this uncertainty. They know that fear or confusion keeps homeowners from refinancing, switching, or shopping for better options. But if you:

- Signed your mortgage between 2020–2022 when rates were ultra-low

- Have 6–24 months left in your current term

- See that interest rates are stabilizing or falling

… then now is the time to assess your position. Because in many cases, even with a penalty, you may save money, unlock equity, or gain the flexibility you didn’t get when you first signed.

This post will help you:

- Understand how prepayment penalties actually work

- See real examples with Saskatchewan context and math

- Decide if breaking early makes sense in your situation

- Avoid the trap of blindly auto-renewing at your bank’s default rate

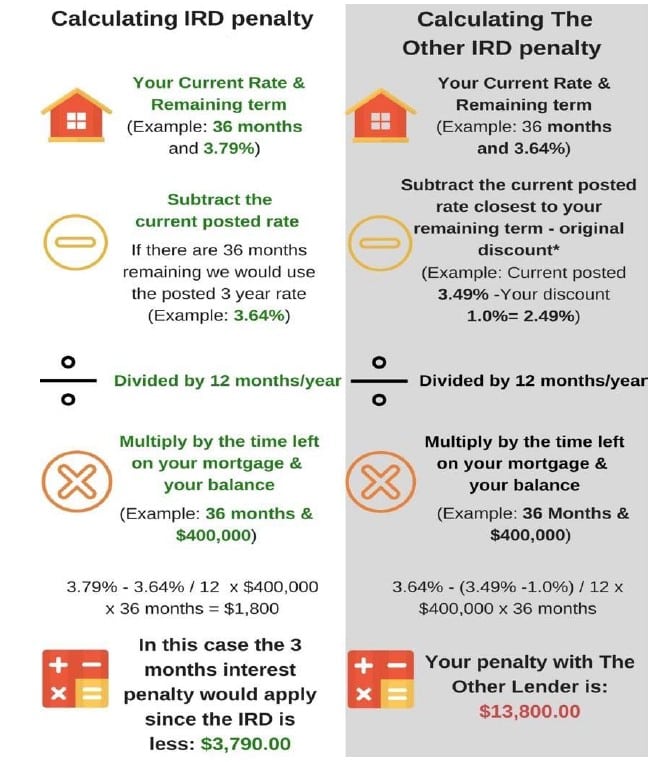

How Are Prepayment Penalties Calculated?

Understand the Math So You Can Make an Informed Choice

Most people know that breaking a mortgage comes with a penalty, but very few understand how that penalty Before You Switch or Break Early

Let’s break down both, with simple explanations and Saskatchewan-relevant examples.

💡 Use our Mortgage Calculator to estimate potential costs and break-even timelines in real time.

For Fixed-Rate Mortgages: It’s Usually the IRD or 3 Months’ Interest — Whichever is Greater

If you’re in a fixed-rate mortgage, your penalty will usually be the greater of:

- Three months’ interest

- Interest Rate Differential (IRD) — this is where it gets more complex

How IRD Works:

The Interest Rate Differential is the amount of interest the lender is losing when you break your mortgage early. The formula varies by lender, but the basic idea is:

Penalty = Mortgage Balance × (Your Rate – Current Rate for Similar Term Remaining) × Time Remaining (in years)

Important: The “current rate” your lender uses is often their posted rate, not the discounted rate you’d actually get — and this is how banks inflate IRD penalties.

Example (Saskatchewan scenario):

- Balance: $325,000

- Current Rate: 2.89% fixed

- Time remaining: 1.5 years (18 months)

- Your lender’s current posted 1.5-year rate: 5.39%

- Discounted market rate: 4.59% ← but your bank might ignore this!

Calculation:

Three months' interest:

= $325,000 × 2.89% ÷ 12 × 3 = $2,348

IRD (if calculated using posted rates):

= $325,000 × (2.89% – 5.39%) × (1.5) → Negative value

BUT if the current rate is lower than your contract rate, IRD applies:

= $325,000 × (2.89% – 1.59%) × (1.5) = $5,940

👉 Your lender will charge the higher: $5,940 IRD

For Variable-Rate Mortgages: It’s Simple — Just 3 Months’ Interest

If you're in a variable-rate mortgage, the prepayment penalty is almost always just three months’ interest — and calculated at your current rate.

Example:

- Balance: $325,000

- Variable rate: 6.00%

- Three months’ interest =

$325,000 × 6.00% ÷ 12 × 3 = $4,875

Why this matters:

In many cases, variable-rate holders pay lower penalties, which is why brokers sometimes recommend variable rates for flexibility — especially for clients who plan to sell or refinance before 5 years.

Why You Need Your Broker’s Help

Most lender websites only show a rough calculator — and they won’t tell you:

- What rates they’re using behind the scenes (posted vs. discounted)

- Whether you’ll actually come out ahead

- If there’s a blended rate option that avoids the penalty altogether

💡 I can request your lender’s official payout statement, calculate your penalty, and compare it to your refinance or switch savings — all before you make a decision.

Real-World Scenarios: Is Breaking Actually Worth It?

The biggest myth about mortgage penalties is that they’re always bad. In reality, there are plenty of situations where breaking early can save you thousands of dollars, or give you access to financial tools you didn’t have when you signed.

Here’s a visual example of how this works:

Let’s walk through two real-world client-style examples — based on Saskatchewan homeowners — so you can see how the math works.

Scenario 1: The Early Switch + Equity Strategy

Client: David & Kendra, homeowners in Saskatoon

Mortgage: $375,000 3-year fixed @ 2.89% (signed July 2022)

Term Remaining: 13 months

Balance: ~$340,000

Penalty: $2,850 (IRD)

New Rate Available: 4.69% 5-year fixed

Goal: Refinance to access $30,000 equity and lower total interest cost

Situation:

- They have credit card and car loan debt totaling $28,000 at 17.99% and 9.5% respectively

- Their home is now worth ~$465,000

- Their current bank offered a 5.39% renewal with no flexibility or early options

Refinance Outcome:

- New mortgage balance: $370,000

- New rate: 4.69%

- Penalty paid upfront from equity: $2,850

- Monthly payment increase: $150

- Total interest saved over 5 years: ~$7,600

- Debt interest eliminated: ~$6,300/year × 5 years = ~$31,500 saved

Total 5-Year Benefit: ~$39,000 in interest savings and debt relief — even after paying the $2,850 penalty.

Scenario 2: The Break + Reamortization Strategy

Client: Jordan, single homeowner in Prince Albert

Mortgage: $265,000 variable rate at 5.75% (signed January 2023)

Term Remaining: 3 years

Balance: $247,000

Penalty: ~$3,562 (3 months’ interest)

Goal: Switch to a new lender, extend amortization, reduce monthly payments

Situation:

- Jordan is expecting a job transition and wants to reduce monthly expenses for 12–18 months

- Home value has increased to ~$310,000

- Jordan is eligible for a 30-year amortization at a lower rate with a new lender

Refinance Outcome:

- New rate: 4.89%

- New amortization: 30 years

- Monthly payment reduction: $245/month

- Total cost of penalty: ~$3,562

- Savings in monthly payments over 2 years: $245 × 24 = $5,880

- Net short-term cash flow improvement (after penalty): ~$2,300

Key insight: It’s not just about rate — restructuring your mortgage through early refinancing can also give you breathing room, especially during life transitions.

💡 See if you qualify to use your equity or reamortize for breathing room.

Summary: When Breaking Your Mortgage Can Make Sense

| Situation | Benefit |

| Rates have gone down | Lower total interest over your new term |

| You need equity | Use your home value for debt consolidation or major purchases |

| You want to restructure your mortgage | Longer amortization = lower payments |

| You’re unhappy with your lender | Switch to better terms, service, or features |

Breaking your mortgage isn’t just about escaping — it’s about unlocking options. A short-term penalty may be the gateway to a better long-term plan.

Strategic Considerations Before You Break or Refinance

Don’t Just Look at the Rate — Look at the Full Picture

It’s easy to get fixated on interest rates — but the smartest mortgage decisions happen when you look beyond the rate. Whether you’re thinking of breaking your mortgage early, refinancing, or switching lenders at renewal, here are the major factors you and your broker need to assess.

1. Penalty vs. Savings: Run a Break-Even Analysis

Don’t guess. Ask your broker to run the real numbers. They’ll compare:

- Your current rate and remaining balance

- What rate you could get now

- The prepayment penalty from your current lender

- How long it will take to recoup the penalty through monthly savings

Formula Example:

If the penalty is $3,000 and you’d save $180/month on the new rate → break-even is ~17 months

→ If your new mortgage term is 5 years, you’ll save over 40 months

If you’re planning to stay in your home for 2+ years, a refinance often makes financial sense — even with the penalty.

2. Are You Accessing Equity the Smart Way?

If your home has increased in value, breaking your mortgage could unlock equity you didn’t have before.

| Equity Use | Smart If... |

| Debt consolidation | You’re carrying high-interest loans or credit cards |

| Renovations | You’re increasing your home’s value or adding rental potential |

| Investments | You’re working with an advisor or building passive income |

| Emergency fund | You need stability or predictability after a life event |

With home prices up in Saskatoon and across much of Saskatchewan, many homeowners now qualify for larger mortgage amounts at lower blended rates.

3. Structure Your Mortgage Based on Life, Not Just Rates

Ask yourself:

- Are you planning to move, upsize, or downsize in the next 3–5 years?

- Are you considering starting a business, growing your family, or retiring?

- Would you benefit from flexible features like lump sum prepayments or skip-a-payment?

Sometimes a slightly higher rate with better terms (e.g., no collateral charge, good portability, 20% prepayment privileges) is a smarter long-term choice than the lowest advertised offer.

4. Not All Lenders Are Equal — Watch for Traps

Banks and alternative lenders vary wildly in how they calculate penalties, apply fees, and handle exits. See CMHC mortgage guidelines for more info. Here are red flags:

| Watch Out For | Why It Matters |

| Collateral charge mortgages | Harder (and costlier) to switch later |

| Low-rate “teasers” | Often come with brutal penalties or restrictions |

| Short rate holds | Could expire before your file is ready to close |

| Limited prepayment terms | Restricts ability to pay down faster |

That’s where I come in — I’ll walk you through rate AND risk so you don’t get stuck later.

5. Timing Matters: Don’t Leave It Too Late

If your mortgage is up in the next 3–6 months, now is the time to act.

- Most lenders allow you to hold rates for 90–120 days

- A refinance or switch can take 3–4 weeks to complete

- Your broker can request a payout statement and review options before you commit

Don’t wait for your lender to auto-renew you at a posted rate with no advice.

Conclusion: Don’t Let Penalties Scare You — Let Them Empower You

Mortgage penalties are one of the most misunderstood parts of homeownership — and for good reason. Lenders don’t exactly go out of their way to explain how they work or when breaking your mortgage might actually be in your best interest.

But now you know the truth:

- Penalties aren’t just fees — they’re tools you can leverage for better rates, debt relief, equity access, or lower payments

- With expert analysis, you can save more over time even after paying a penalty

- Acting before your renewal window gives you the most flexibility, the most options, and the most control

The biggest mistake? Waiting. Letting your mortgage renew on autopilot. Ignoring the fine print. Leaving thousands of dollars on the table because it felt “easier” to do nothing.

Ready to see if breaking your mortgage makes sense?

✔️ Let’s run the numbers

✔️ Review your lender’s payout details

✔️ Compare new options side by side

📧 Email: mike@huysmortgagegroup.com

📞 Call or text Mike at (306) 281-4084