It’s More Than Just the Interest Rate: What Every Homeowner Should Know About Mortgage Renewals

Hi, I’m Mike, and if you’re here, chances are you’re thinking about renewing or refinancing your mortgage. Most people focus on one question: What’s the lowest rate I can get? While that’s an important factor, there’s much more to the story.

Your mortgage is more than a number—it’s a key piece of your financial puzzle. Making the right choice depends on your unique goals, whether that’s lowering monthly payments, paying off your mortgage faster, or preparing for a life change like moving or renovating. Let’s dive into what you need to know to make the best decision for your situation.

Renew vs. Refinance: What’s the Difference?

Before we get into the details, it’s important to understand the difference between renewing and refinancing:

- Renewing: When your mortgage term ends, you can renew with your current lender or shop around for a better deal.

- Refinancing: Can be done during or at the end of term, often to access equity, consolidate debt, lock into better terms or extend amortization.

Both options have benefits, but your choice should align with your financial goals.

It’s Not Just About the Rate: Hidden Costs to Watch For

While a low rate may seem like the obvious choice, there are often hidden costs that can impact your bottom line.

Early Cancellation Fees

If you’re refinancing before your term ends, your lender may charge penalties. These penalties can be significant, depending on your mortgage type and remaining term. For example, fixed-rate mortgages often have higher penalties than variable-rate ones. You can calculate your penalties, using RateHub’s Mortgage Penalty Calculator.

Porting Your Mortgage

Are you planning to move in the next few years? If so, make sure your mortgage is portable. Porting allows you to transfer your existing terms to a new property, saving you from penalties. Not all lenders offer this feature, so it’s worth asking your broker.

Amortization Adjustments

Refinancing may reset your amortization period. While this could lower your monthly payments, it can also mean paying more interest over time. If your goal is to pay off your mortgage faster, this is something to consider.

Fixed vs. Variable Rates: One Size Doesn’t Fit All

Deciding between fixed and variable rates is like choosing between stability and flexibility. Here’s a quick breakdown:

- Fixed Rate: Consistent payments make it easy to budget, even when interest rates fluctuate. This is a good option if you prefer stability, but you might miss out on savings if rates drop.

- Variable Rate: These typically start lower, but they’re tied to market conditions, so your payments could increase. Variable rates offer more flexibility but come with an element of risk.

What Are Your Goals?

The right mortgage isn’t just about the numbers; it’s about what fits your life. Here are a few scenarios to consider:

- Growing Families: If you’re expanding and need more space, refinancing to access equity for a bigger home or renovations could be a smart move.

- Condo Owners: If your building is planning major upgrades, like replacing the roof, refinancing could provide the funds you need.

- Newcomers: If you’re new to Canada, navigating the mortgage process can be overwhelming. A broker can help you understand your options and find a mortgage that works for your needs.

- Retirees: If you’re downsizing or looking to pay off your mortgage faster, you’ll want a solution that offers flexibility without unnecessary fees.

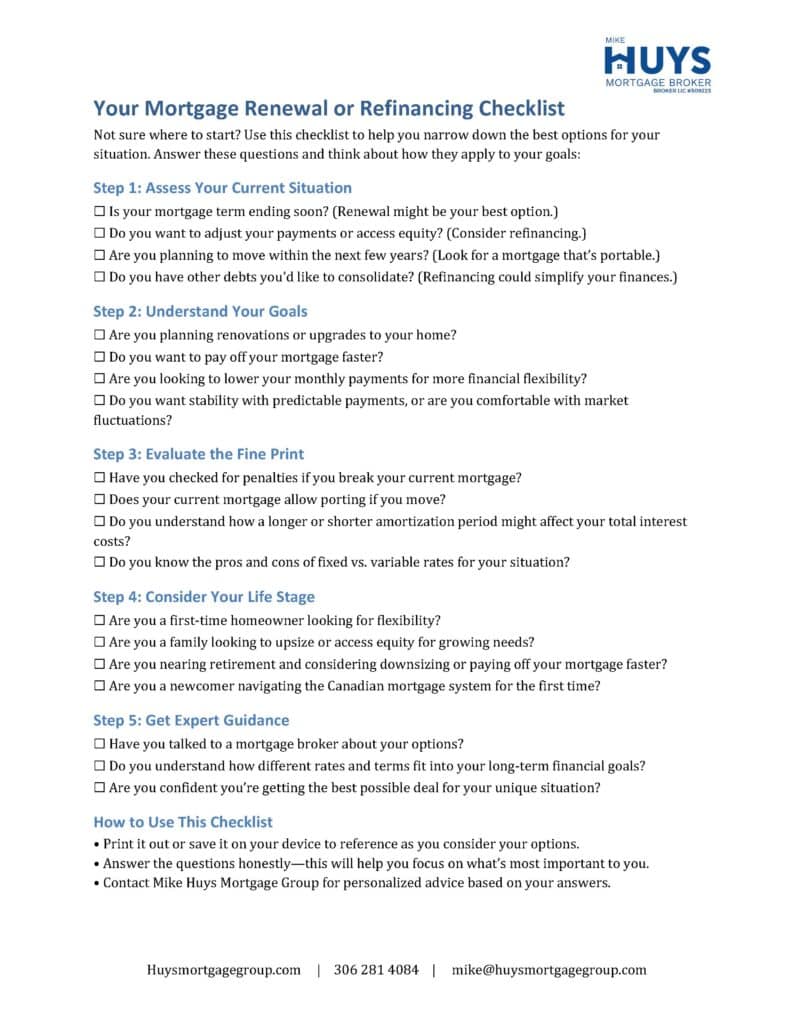

To help you with your goals and mortgage rate decision-making process, I’ve put together a checklist to help you narrow down the best options for your situation. You can download it by clicking the image below.

A Prairie-Perfect Mortgage Analogy

Your mortgage is like a trip to the Saskatoon Farmers’ Market. You might be tempted to grab the cheapest loaf of bread, but if it’s not fresh or doesn’t meet your needs (like gluten-free or whole grain), it might not be the best choice. The same goes for mortgages—sometimes paying a little more or choosing a better fit makes all the difference.

Resources for Saskatoon Homeowners

Here are some helpful tools and resources to guide your decision-making:

- Mortgage Payment Calculator

- City of Saskatoon Property Tax Assessment

- Understanding Mortgage Penalties (RateHub)

- Fixed vs. Variable Rates (RateHub)

Why Work With a Broker?

No matter your stage in life, mortgage decisions can feel overwhelming. As a broker, I’m here to simplify the process and find the best options for you. Unlike banks, I have access to multiple lenders and products, ensuring you get terms that align with your goals.

Think of me as your mortgage guide, here to help you navigate the twists and turns, avoid hidden costs, and find a solution that works for your unique situation.

The Bottom Line

Your mortgage should be more than just a number. It should support your goals—whether that’s paying off your home faster, upgrading to your dream property, or staying financially flexible.

If you’re renewing or refinancing, let’s chat. Together, we’ll look at the big picture and find a solution that works for you, your family, and your future.